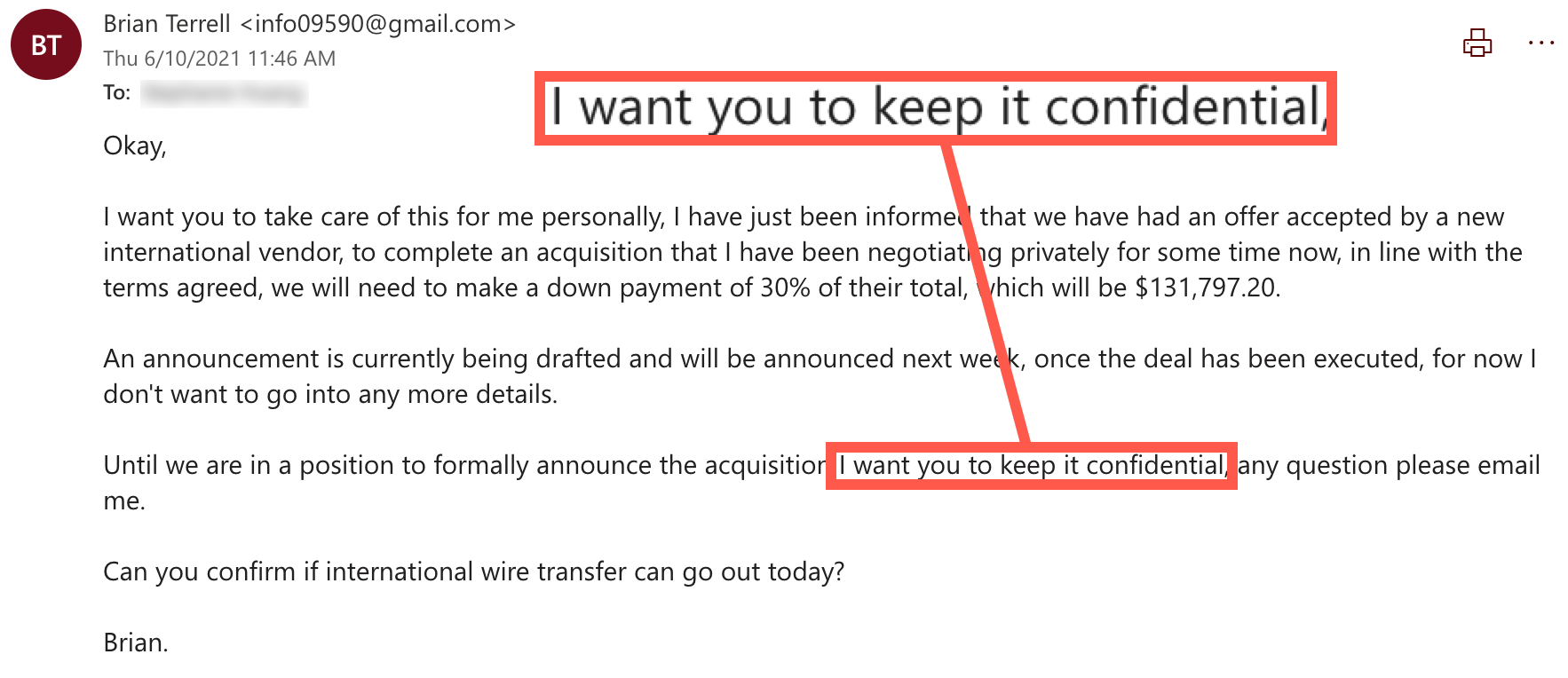

Ransomware is the business continuity issue of our time.

Everyone is a target, and this 3 minute and 30 second video shares exactly how I was targeted last year:

Tags: Quickbooks upgrade, Intacct, Quickbooks, outgrown Quickbooks, Sage Intacct, BTerrell SmartSuite

Tags: Quickbooks upgrade, Intacct, Quickbooks, outgrown Quickbooks, Sage Intacct, BTerrell SmartSuite

Tags: Quickbooks upgrade, Intacct, Quickbooks, outgrown Quickbooks, Sage Intacct, BTerrell SmartSuite

Tags: Quickbooks upgrade, Intacct, Quickbooks, outgrown Quickbooks, Sage Intacct, BTerrell SmartSuite

Tags: Quickbooks upgrade, Intacct, Quickbooks, outgrown Quickbooks, Sage Intacct, BTerrell SmartSuite

Need Help to Get Started with Sage Intacct?

|