They say that pain is the touchstone of all spiritual growth. Maybe of business growth, too. A CFO at a major client experienced some real challenges around the normally unremarkable task of Form 1099 compliance that taught both her and me some best practices on this subject. I thought I'd share them here.

Read More

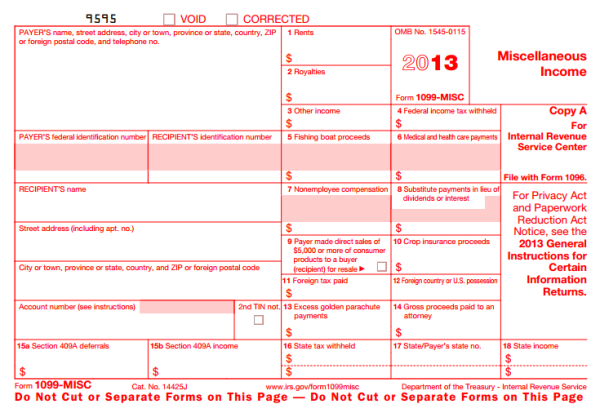

If anecdotal evidence counts for anything, the IRS may be stepping up their efforts at Form 1099 annual filing compliance. Recently, we heard of one mid-sized company that was fined around $25,000 for not completing the Recipient's Name correctly in an electronically filed batch. $25,000 is a lot of money, especially when it relates to a batch of 40 or so records. Do the math...that's $625 per form. Perversely, it seems that maybe they were just trying to ensure that the fine was greater than the annual filing baseline of $600 in service payments (and a host of other types of payments). Actually, they were following a formula that mandates a per form penalty for various offenses starting at $30 per form up to $250 per form. The maximum penalty starts at about $500,000 for small businesses, but there is no maximum under certain conditions. Payer beware!

0 Comments Click here to read/write comments

Tags: 1099, 1099 reporting, 1099 compliance, aatrix